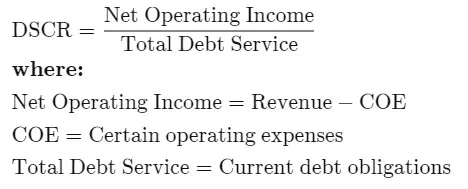

- The debt-service coverage ratio loan (DSCR) is a measure of the cash flow available to pay current debt obligations.

- DSCR measures a business’s cash flow versus its debt obligations.

- Lenders use DSCR to determine whether a business has enough net operating income to pay back the loan debt.

DSCR – Debt Service Coverage Ratio Loans

DSCR Loans

A DSCR loan is a mortgage loan secured by a residential income-producing property used for a business purpose.

- It is primarily based on the “Debt Service Coverage Ratio” or the “Cash Flow” of the property rather than the borrower’s income.

- DSCR measures a firm’s available cash flow to pay current debt obligations.

Let's Start your Investment Journey And Finance Your Dream income-Producing Property

- A traditional mortgage loan will require income verification, tax returns and a “Debt-to-Income” (DTI) ratio. DSCR Loans do not require income verification from the borrower (Investor).

- “Business Purpose” = DSCR loans strictly do not allow the owner of the property to live in the property. It must be used for “Business” or Investment purposes.

- DSCR loan financing cannot be utilized to purchase primary or secondary residential homes

Key Takeaways

Investment Opportunities Await!

- Formula: DSCR equals net operating income divided by debt service, including principal and interest. (Rental income from the property / PITIA – Principal, Interest, Taxes, Insurance and HOA if application payment)

- A DSCR of 1% indicates the property can generate exactly enough operating income to pay off its debt service costs. Therefore, the higher the % the better.

- A DSCR less than 1% reflects a negative cash flow, and the property and/or owner may be unable to cover or pay current debt obligations without depending on outside sources.

Requirements

What is Required to Obtain A DSCR Loan?

Max Loan-to-Value (LTV) Ratio

85% LTV max; First time Investors max may be as low as 70% requiring the Investor to pay a down payment equal to 30%. All depending on Lender guidelines, credit score, loan transaction type (Purchase or Refinance)

Multi-Unit Properties

1-4 Family homes (SFR); 2-4 Unit properties (Multi-family)

Condos and townhomes are permitted

Loan Limits

Minimum Loan Amount: $100k

Maximum Loan Amount: Up to $3M – depending on the Lender

Minimum FICO Score required: 620

A 640 is most common and a 680+ offers better pricing

Some Lenders may require a 680+ minimum FICO score for 1st time Investors.

Assets

Most recent bank statement covering 30 days history sourced and seasoned funds available

Max Seller Concessions: 2%

Income

No Income documentation or verification is required.

Gift Funds

Gift funds allowed with 5% of borrowers own funds or 100% gift funds allowed there will be a LTV 10% reduction